AI Bubble or Real Growth? What the 2026 Data Actually Shows

Is AI the biggest opportunity of our time, or the next dot-com bubble waiting to burst? Both sides have strong arguments. Here is a fair, neutral look at the real numbers — and a simple way to think about it.

If you don’t have time to read, then listen to a podcast.

Two stories, both backed by real evidence

Every few weeks, the news swings between two headlines. One says that artificial intelligence is a giant bubble about to pop. The other says AI is the biggest growth story of a generation. The truth is that both sides have genuine, fact-based arguments — and a careful investor should understand both before forming a view.

In this article, we lay out the four strongest points on each side, using the latest 2026 data. We do not tell you what to think. We simply show you the evidence so you can judge for yourself.

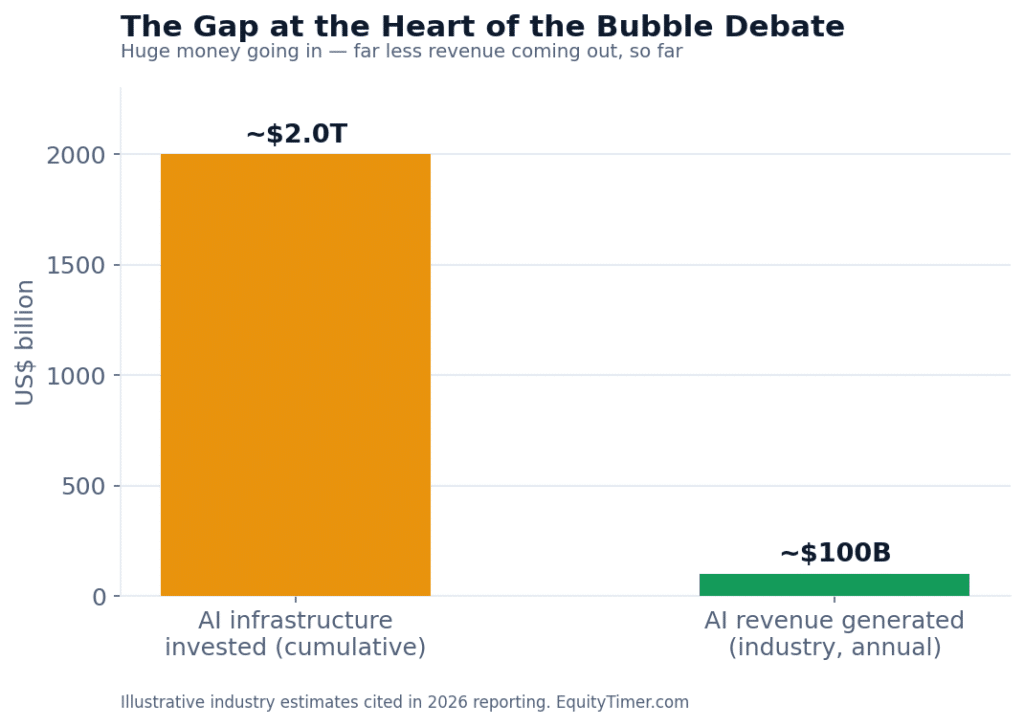

Figure 1: The single chart at the center of the debate — a very large amount of money has gone into AI infrastructure, while the revenue it has produced so far is much smaller. Figures are illustrative industry estimates cited in the 2026 reporting.

The case for a bubble (4 points)

1. Spending is far ahead of revenue. The world’s biggest technology companies are spending enormous sums on AI — hundreds of billions of dollars a year — yet the revenue directly generated by AI remains small by comparison. If that gap does not close, the spending becomes hard to justify.

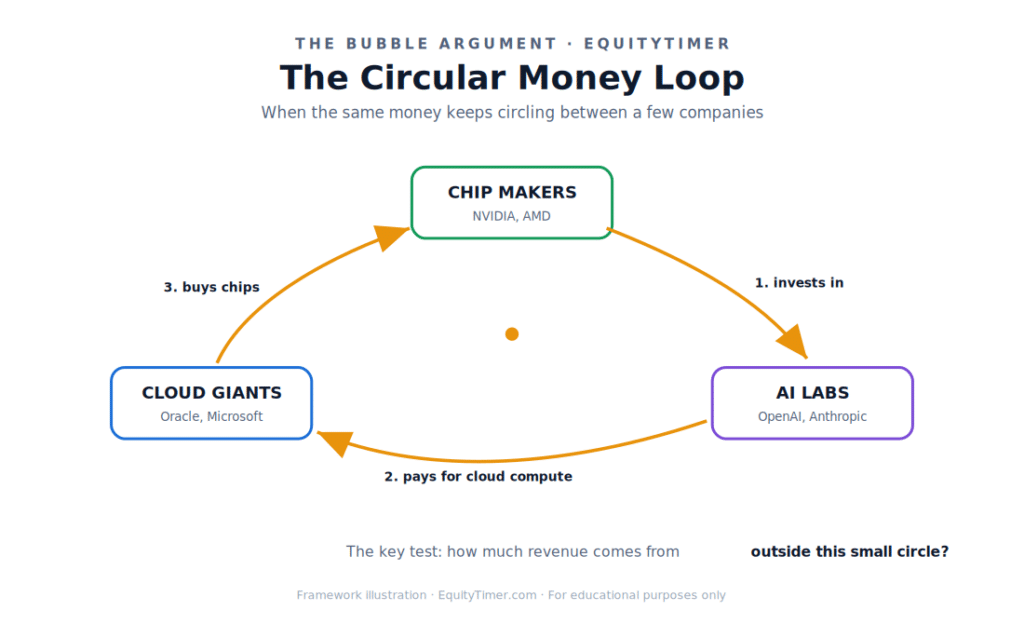

2. The money may be going in circles. A common worry is that the same money keeps moving between a small group of companies: chip makers invest in AI labs, the labs pay cloud companies for computing power, and the cloud companies buy more chips. If most of the revenue comes from within this small circle rather than from outside customers, the growth can appear larger than it really is.

Figure 2: The “circular money flow” concern. The key question is how much revenue comes from outside this small group of companies.

3. AI is getting cheaper fast. When a Chinese lab released a model that performed nearly as well as top US models at a small fraction of the cost, it raised a serious question. If AI keeps getting cheaper and better every year, the huge spending on today’s expensive infrastructure may not be needed for long.

4. Land and power are real limits. Building giant data centers needs land, water, and electricity. In several places, projects have been delayed by public objections, court cases, and grid constraints. These are practical, physical limits that money alone cannot quickly solve.

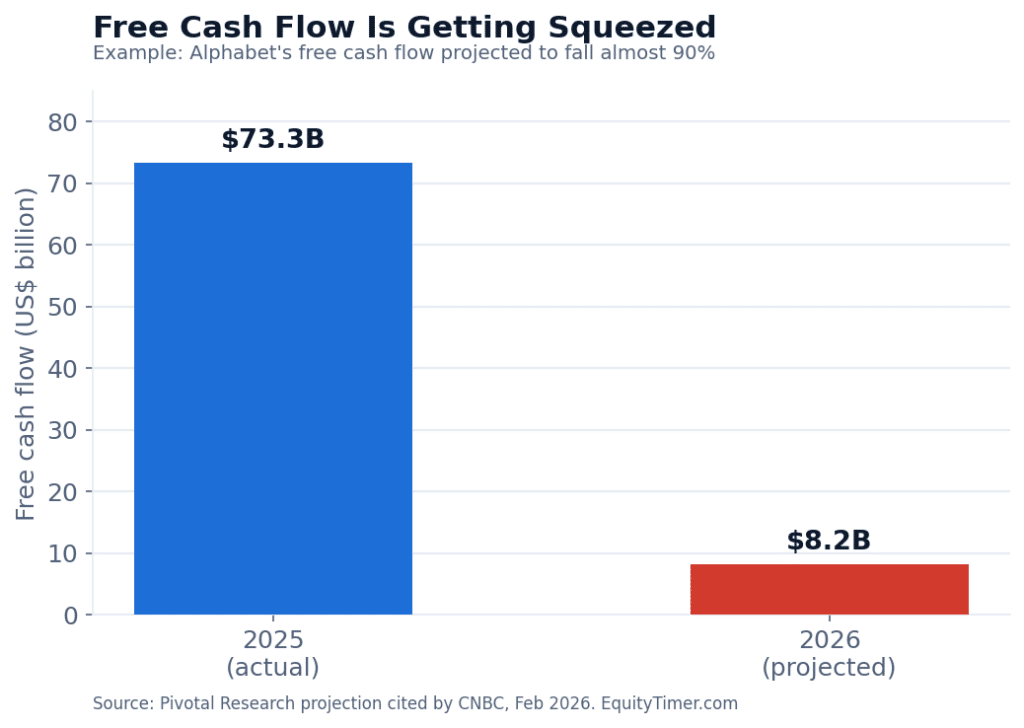

Figure 3: One sign of the pressure — Alphabet’s free cash flow is projected to fall almost 90 percent in 2026 as AI spending rises. Source: Pivotal Research projection cited by CNBC, February 2026.

The case for real growth (4 points)

1. This is not the dot-com era. In 2000, many bubble companies had no real business. Today, the leaders do. Amazon’s and Google’s cloud divisions already earn substantial, real revenue and are profitable. They are investing in AI for future growth from a position of strength, not desperation.

2. The next version of AI is much bigger. The first wave of AI was a simple chat box. The next wave is “agents” — AI that does multi-step work on its own. By one major bank’s estimate, an agent-based task can need many times more computing power than a simple chat query, which means demand could keep rising sharply.

3. Real results are already showing. This is not only a theory. Companies using AI in everyday tools — from office software to customer service — are reporting faster work and real productivity gains. When a technology saves time and money in the real world, its demand tends to persist.

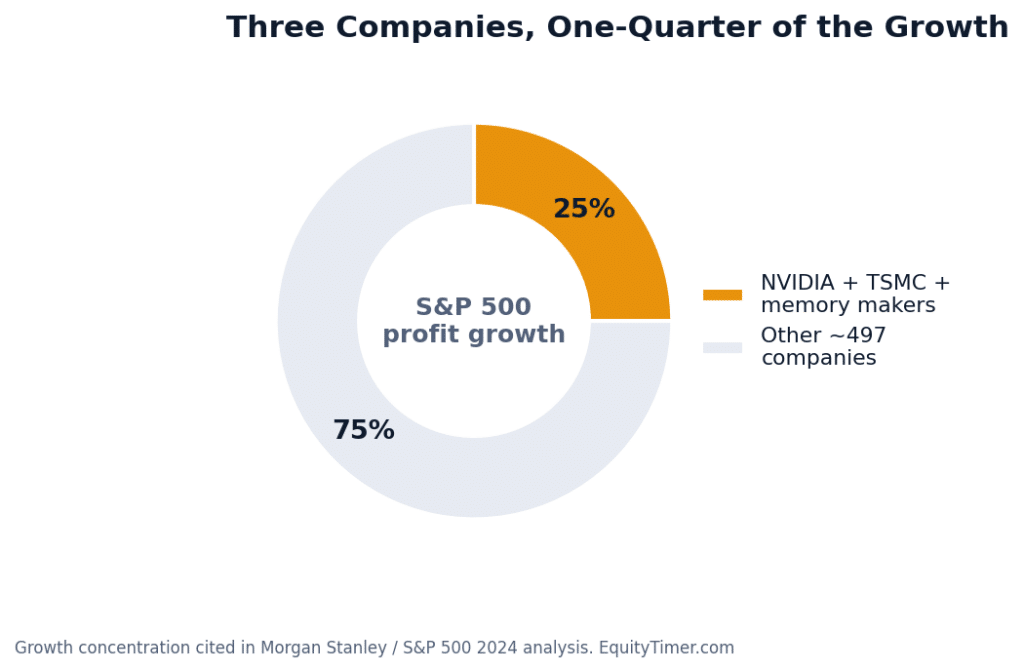

4. The chip makers’ cash is real. Whatever happens to the AI labs, the companies selling the “pickaxes” are earning real money now. According to one analysis, a small group of chip and memory companies accounted for around a quarter of the S&P 500’s expected profit growth in a single year.

Figure 4: Profit growth is highly concentrated — a handful of chip and memory companies drove roughly a quarter of the S&P 500’s expected profit growth. Source: figures cited in 2026 Morgan Stanley / market analysis.

Bubble vs growth: side by side

Here are both sets of arguments in one simple table, so you can weigh them together.

| The bubble case | The growth case |

| Spending is far ahead of AI revenue so far | Cloud divisions already earn real, profitable billions |

| Money may be circling among a few companies | Next-gen “agent” AI needs far more computing power |

| AI costs are falling fast, so today’s spend may be wasted | Real productivity gains are already showing up |

| Land and power limits are stalling real projects | Chip makers’ cash flow is real and visible today |

Table 1: A neutral summary of both arguments. This is for education only and is not a recommendation either way.

A neutral, practical view

Putting both sides together, a balanced view looks like this. The bubble risk is real — but mainly for companies burning cash and whose returns remain unproven. The companies with the strongest position are the ones selling the “pickaxes” and the cloud capacity, because they have real orders and real cash flow today.

In other words, “Is AI a bubble?” is the wrong question. A better question is: which specific companies have real customers and real cash now, and which are valued only on a promise? The first group can survive a slowdown. The second group is where the real risk sits.

Before making any decision, the sensible steps are the same as always: look at the free cash flow, check whether it is positive, and understand exactly how the company makes money. If AI really is a ten-year story, there will be time to invest carefully rather than chase the hype.

More in this series

Part 1 — The 5 Types of AI Companies. Where the money flows, layer by layer.

Part 3 — How to Invest in US AI Stocks from India. The LRS route, fractional shares, and taxes.

Frequently Asked Questions (FAQ)

Is AI a bubble in 2026?

There is no firm consensus. There are strong arguments on both sides. The bubble risk is highest for companies spending heavily with unproven returns, while companies with real cash flow today, such as chip and cloud firms, look more solid. This article is for education only and is not investment advice.

Why do people compare AI to the dot-com bubble?

Because both involved huge investment and high excitement. The key difference is that today’s AI leaders often have large, real, and profitable businesses, whereas many dot-com companies in 2000 had little real revenue.

What is the “circular money flow” concern?

It is the worry that the same money keeps moving between a small group of companies — chip makers, AI labs, and cloud providers — rather than coming from outside customers. If true, it can make AI growth look larger than it really is.

How can I tell a real AI business from hype?

A simple test: does the company have real customers paying real money today and generating positive free cash flow? Companies that only promise future AI earnings carry more risk than those already earning cash.

Does the AI debate affect Indian investors?

Yes, indirectly. Most large AI companies are listed in the US, and Indian investors can access them through the LRS route. The same caution applies: understand the business and the risks first. We explain the practical steps in Part 3 of this series.

Disclaimer

EquityTimer is an educational resource and is not registered with SEBI as an investment adviser. Nothing in this article is investment advice, nor a recommendation to buy, sell, or hold any security. Company names and figures are used only for illustration and analysis. All data is taken from public company filings and reputable financial press as of June 2026 and may change. Please do your own research and consult a SEBI-registered adviser before investing.